How credit scores work

Your credit score is a summary of your credit history. A credit score is simply a prediction of how likely you are to pay back a loan. It’s often a three digit number between 300-850 where 850 represents the best chance of repayment. If your credit report is a report card, your credit score is your grade.

Myth: You have one single credit score.

Often people will describe their credit score as a single number, but you should be aware that there isn’t a single credit score— there are multiple credit scores. You might access your credit score through a credit monitoring service, and they’ll tell you a number—but in reality, that’s just at one point in time on a single scoring model.

The two most common credit scores are models from FICO and Vantage, but even within those there are different model versions and even specific models for auto loans or other specific lending types. On top of that, many lenders will calculate their own custom score rather than using one FICO or Vantage score.

What this means for you: because there are different scores, what you’re doing to improve your credit score might not have the same impact on each score type.

Your credit score is important, but it’s not a single number.

FICO and Vantage chose the same scoring system, from a low of 300 to a high of 850. However, they each interpret the grades a little bit differently. For example, to be considered having “Good” credit you need to have a Vantage score over 700 or a FICO score over 670.

Myth: Everyone has a credit score.

Myth: Everyone has a credit score.

Not everyone has a credit score. Some people have a credit bureau history and not a score, and some people don’t have credit history at all. Not having any credit history or having very limited credit history can be as challenging has having negative credit history.

If you don’t have any credit bureau record, you are considered “credit invisible”—that means lenders don’t have access to any information about you. Many customers, though, do have a bureau record but not enough credit history to have a credit score. They are considered “unscorable”.

Without a credit score, customers who are invisible or unscorable often find it difficult to get a loan or credit card, and often get similar products and interest rate/fees as customers who have low credit scores.

Myth: If you're credit invisible of unscorable, there's no real way to build credit without trapped in debt.

If you fall into one of these categories, there are actually a number of ways to establish credit history: New (free!) Bureau offerings have emerged that allow you to establish a bureau profile directly or to furnish data to the bureaus to expand your credit file. Experian GoTM and Experian BoostTM are specifically designed for this. With your permission, they can start using bill payments and rent payments to build your credit history.

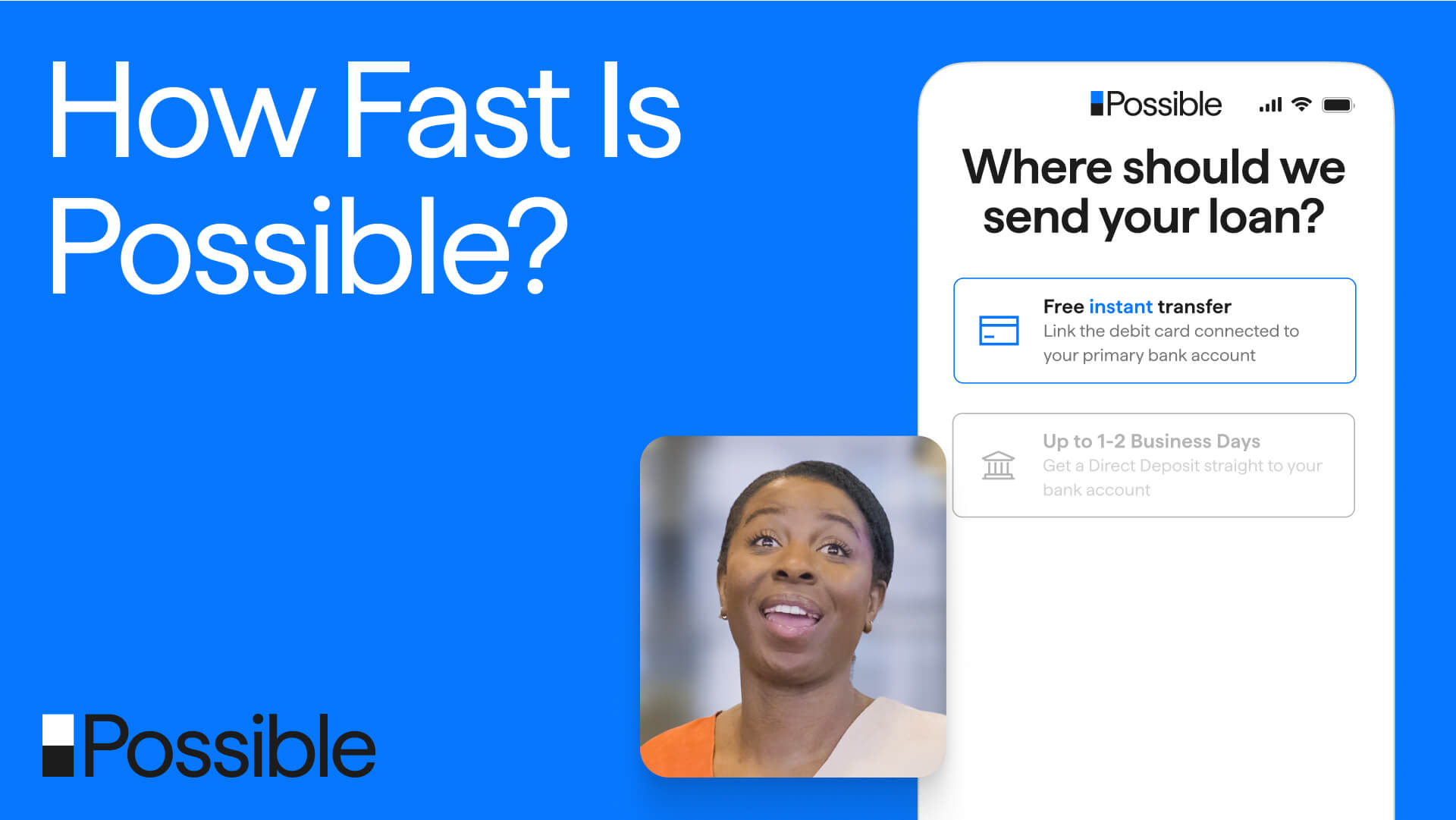

There are also financial products that will use non-bureau data to allow you to be approved without credit history, typically using your employment and income/bank data. Possible does this, too.

There are also secured card offerings that give you credit against a sum of money that you hold in a deposit account. Many neighborhood banks do this, too. Whenever you’re taking out a loan or a credit card for the purpose of building credit, be aware of the cost of the product and make sure the company actually reports to credit bureaus.

Beyond these myths, there’s so much more to learn about credit. As part of our commitment to our customers’ financial wellbeing, this financial literacy series will break down these topics. Our mission at Possible is to help you end the debt trap and unlock economic mobility for good. 🟦